Coal in 2025: the most new power plants in 10 years, but less electricity from coal.

Global Energy Monitor (GEM) released an annual report on global coal. Two concurrent trends show that capacity and generation diverge: worldwide the most new coal power plants were built in 10 years (97 GW ≈ ~100 large units), but coal electricity production worldwide fell by 0.6 %.

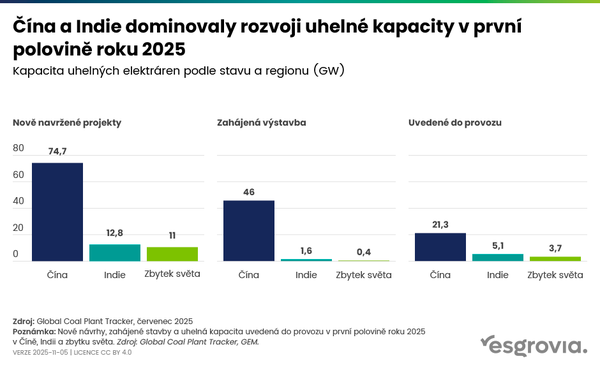

95 % of new coal power plants built in China and India (vs. 87 % in 1H 2025):

🇨🇳 China: +78 GW capacity, but generation -1.2 %

🇮🇳 India: +10 GW capacity, but generation -2.9 %

Outside China and India, only 32 countries are building coal (vs. 38 in 2024), a total of 9 GW combined.

The key paradox is that we have more capacity but lower utilization – each new coal power plant in China/India operates for increasingly less time.

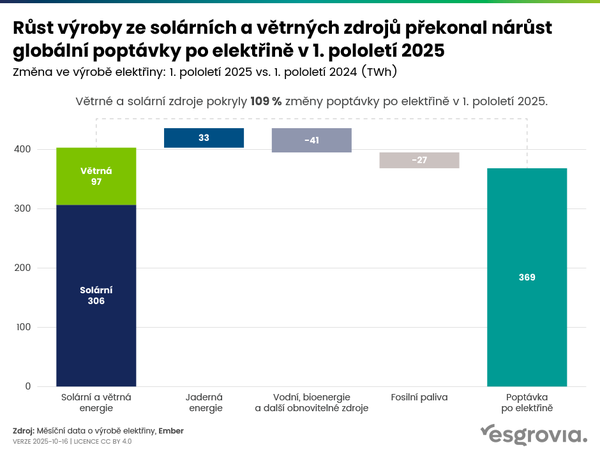

Solar and wind energy cover most/all of the demand growth in both countries.

Other countries are withdrawing from the coal market – South Korea, Brazil, Honduras pulled their new coal plans in 2025, Latin America now has no new coal proposals, and, for example, in Turkey only 1 out of 70 proposals from 2015 remains.

Construction of new coal power plants is concentrated in China (in 2025 it proposed a record 162 GW of new coal projects), India (plans to complete 85 GW in the next 7 years), Indonesia (partly due to processing nickel and aluminium for battery production) and Zimbabwe + Zambia (2/3 of planned coal in Africa).

In the Western world, the phase‑out of coal is also being delayed – 70 % of coal units that were supposed to close in 2025 did not close:

🇪🇺 EU: 69 % shifts due to the 2022–2023 energy crisis. But coal generation in the EU is still 40 % below 2022 levels.

🇺🇸 USA: 59 % retirements cancelled – Trump "emergency orders" keep 5 coal plants online for hundreds of millions of USD, households paid +7 % on electricity.

What to take away from this?

1. Capacity ≠ generation = a new coal paradigm. New coal capacity is still being built, but there is less and less time left. This erodes the economics of every plant and creates a stranded asset already at commissioning. A key shift for energy investors.

2. China/India narrative vs. reality. "China and India are building coal" is true, but it’s not the whole picture. Both countries are simultaneously driving global solar/wind expansion. China’s 15th Five‑Year Plan (2026–2030) also pledged to "promote peaking" coal. It’s not a coal renaissance, but a temporary buffer with a fast exit path.

3. The Indonesian detail is important: 25 % of new coal power plants serve nickel and aluminium processing for battery production. Coal energy therefore paradoxically powers the green transformation elsewhere, something like a "dirty battery for a clean West".

4. The impact of the Iran conflict should be short‑term. Eight countries announced plans to increase coal use because of Iran, but GEM and Carbon Brief expect the "return to coal" to be limited. Historically, oil/gas price volatility paradoxically accelerates the shift to renewables more than it slows it down.

5. For investors – if we trust GEM, coal infrastructure continues to grow in Asia, but the return on new projects is getting worse. That is structurally negative for coal and positive for renewables.

Related articles

China and India account for 87% of new coal capacity in the first half of 2025

Renewable sources overtook coal as the world’s leading source of electricity for the first time